Economics (definition): a social science concerned chiefly with description and analysis of the production, distribution, and consumption of goods and services

From a slightly more relevant perspective, I would like the definition to simply include the premise of the relationship between supply, demand and price.Nox Rentals is one of the largest luxury villa management companies in Cape Town with around 150 properties under management. We specialise in renting homeowners investment or leisure properties in the short term space. Weve been operating for 15 years, and have enough data to make valid assertions regarding the state of the market.As of the end of 2017, there are a number of market forces at play, specifically on the supply side. The marketplace has formalised over the past 3 years, primarily through the introduction of AirBnB which has brought approximately 17,000 listings onto the platform in Cape Town alone. Added to this, there are 1,500 hotel rooms and apartments being brought into the market in the next 5 years whilst inbound international tourism numbers have been growing steadily at around 15% YOY.

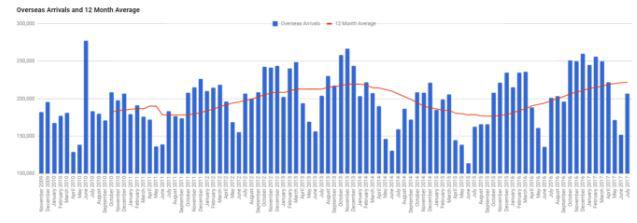

Considering AirBnBs official launch in Cape Town was in July 2015, one can safely say that the private accommodation space has now become an accepted form of travel for guests, and in certain cases, a lucrative investment opportunity for property owners.But, like any trend or gold rush, there are caveats to one successfully benefitting from the new opportunity. With excess supply entering the market, and a notional increase in demand comes a reduction in price. Weve received some calls over the past few weeks from homeowners saying its much quieter this year. Our stats indicate that inbound tourism demand isnt necessarily slower, but occupancies are not as strong as they were last year because of excess supply. This is a natural cycle, and, considering economic principles, demand levels will increase in due course:

Considering AirBnBs official launch in Cape Town was in July 2015, one can safely say that the private accommodation space has now become an accepted form of travel for guests, and in certain cases, a lucrative investment opportunity for property owners.But, like any trend or gold rush, there are caveats to one successfully benefitting from the new opportunity. With excess supply entering the market, and a notional increase in demand comes a reduction in price. Weve received some calls over the past few weeks from homeowners saying its much quieter this year. Our stats indicate that inbound tourism demand isnt necessarily slower, but occupancies are not as strong as they were last year because of excess supply. This is a natural cycle, and, considering economic principles, demand levels will increase in due course: Were currently in the bottom right-hand side quadrant of the above image.

Were currently in the bottom right-hand side quadrant of the above image.